Used Cars, Lumber, and Chipotle Burritos: Let’s Talk Inflation

Used Cars, Lumber, and Chipotle Burritos: Let’s Talk Inflation

Hello friends, and welcome to Young Money! If you want to join hundreds of other readers in learning about finances, career navigation, and figuring this life thing out, subscribe below:

You can check out my other articles and follow me on Twitter too!

- Causes & Effects of Rate on Prices & Interest")

If pandemic was 2020’s buzzword, inflation takes the crown for 2021. From bankers, to construction workers, to restaurant owners, everyone is talking about inflation. Why are used cars so expensive? Why do 2x4s from Home Depot cost so much? Why did Chipotle raise its prices by 4%? Inflation.

What is Inflation?

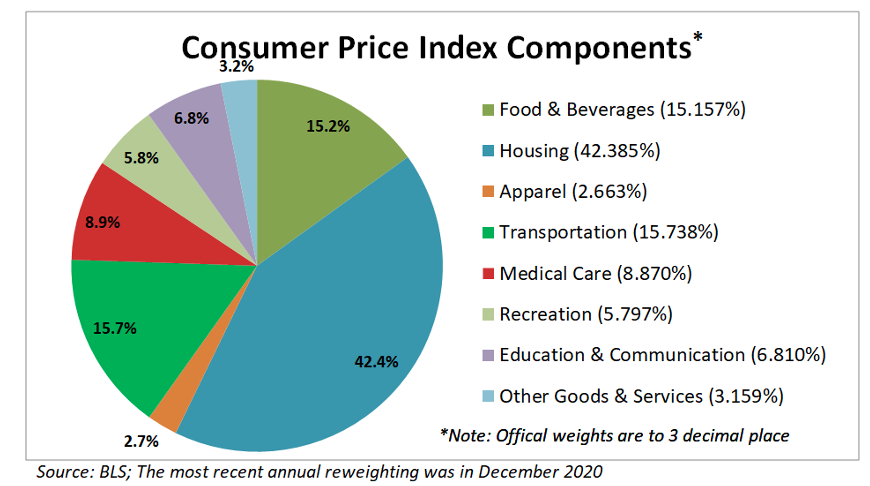

Inflation is the decline of purchasing power of a given currency over time. In the US, we measure this using the consumer price index, or CPI. The CPI contains a variety of consumer goods, as shown below.

To calculate inflation, economists see how much it costs to buy this “basket”, and they compare that cost to prior periods such as last month or last year. The percent increase or decrease is the inflation rate. For June 2021, inflation was 5.4% year over year and 0.9% month over month. What does this mean? If you paid $100,000 for this “basket” last year, it would cost you $105,400 this year. The average inflation rate from year to year is ~2%.

Deflating Your Savings

2% annual inflation doesn’t seem like much, but it compounds over time. Inflation is a shadow tax that will eat away at your savings. Say you have $1,000,000 in a savings account, and you don’t touch it for ten years. If inflation averages 2% over that period, your $1,000,000 in 2021 is only worth $817,072 in 2031 purchasing power. You think you’re being prudent by saving your money, but inflation is eating away at your bank account. This is why I hate savings accounts. By playing it safe, you are guaranteed to lose money over time. Money that you may need over the next year is fine in a savings account, but anything else should be invested.

Investing is the best way to fight inflation. While inflation increases by ~2% a year, the stock market averages 10% returns a year. Investing in the market will yield ~8% REAL returns a year (10% - 2%), while a savings account will yield -2%. If you put $100,000 in a savings account for 25 years, you will be left with $60,346 in purchasing power. If you put $100,000 in an S&P index fund for 25 years, you will have $684,847 in purchasing power. In the long run, savings accounts are far riskier than investments.

Isn’t Inflation Out of Control This Year?

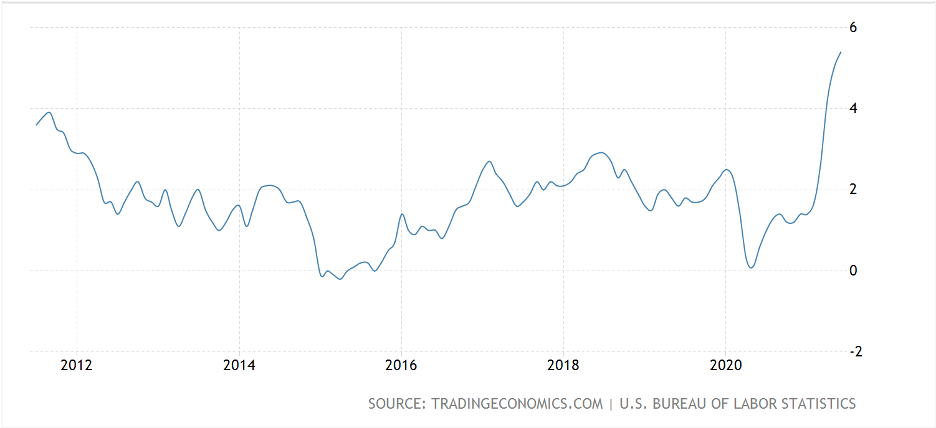

At first glance, yes. June 2021 had a 5.4% year over year and 0.9% month to month inflation rate. This is the biggest jump since 2008. That looks really bad, but it’s probably not that big of a deal. Why? Check out what happened last year:

Annual Inflation Rate: 2011 - 2021

Over the last ten years, inflation was about 2% year over year. When COVID-19 hit, our economy came to a screeching halt. You can see where inflation fell to near 0. Retail shopping was nonexistent, no one was traveling, and countless businesses were shut down. Now America is booming again. Everyone has the travel bug, everyone wants to get back out in the world, and businesses are finally open again. Inflation is a year over year measure. No wonder inflation looks so bad. We’re comparing a wide-open economy to 2020’s lockdown. Economists debate whether or not inflation is transitory (temporary). I think we will see year over year inflation rates normalize as we get farther from last year’s lockdowns.

What’s Driving Inflation?

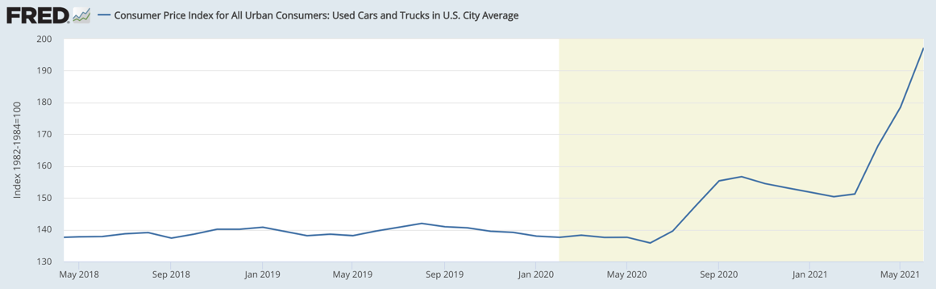

Used cars. Literally. The price of used cars has gone nuts:

Why? Supply issues stemming from COVID-19. Semiconductors are a critical component of new vehicles. When the pandemic started, many auto makers scaled back their semiconductor orders, as they anticipated a drop in demand. The semi manufacturers lowered production in response. Well, demand recovered quickly, and the auto industry wasn’t ready. There are a ton of people who want to buy cars, and there aren’t enough cars to buy thanks to the chip shortage. When customers can’t be new cars, they turn to the used car market.

On top of that, rental agencies like Hertz and Avis sold off part of their fleets last year. With consumer demand roaring back, they have been scrambling to buy as many used vehicles as possible. When everyone wants a car, and there are no cars, prices skyrocket.

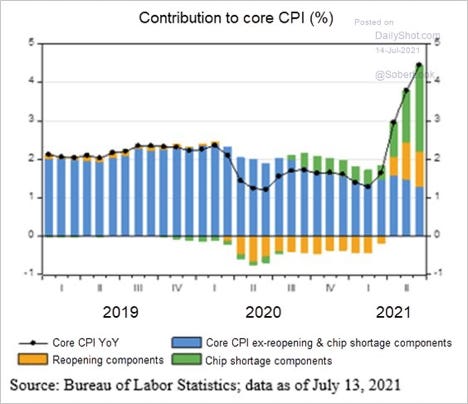

Check out this CPI graph that I found broken down by function. If you remove chip shortage components (auto prices) and reopening components (travel, hospitality, and restaurants), inflation doesn’t look all that bad.

Most of this year’s “inflation” is really the auto and travel/hospitality markets. Obviously inflation will look high when you’re comparing air travel and restaurants to June 2020.

The supply issues affecting the auto market can also be seen elsewhere. Prices of materials like lumber and steel have skyrocketed this year. Saw and steel mills cut production during the pandemic, but construction demand came roaring back quickly. This pattern is visible across several industries: production cuts in spring 2020, unexpected high demand in 2021, high prices as businesses scramble to keep up. These prices should normalize over the next year or so.

Other Components to Inflation

While automotive and reopening components are driving the majority of inflation, there are some other variables at play. Several restaurants such as Chipotle have had to raise their prices in response to wage rate increases. Many restaurants and other small businesses had to lay off employees last year. Some workers took different jobs during the pandemic, some took unemployment benefits, and some may have chosen to retire early. Regardless of the reason, companies are now being pressured to increase wages to hire new employees. While car and material prices will probably regress to their means, wage rate-based price increases are probably here to stay.

Conclusion

Inflation is always going to be here, but that isn’t a bad thing. Wages tend to increase over time with prices. Inflation can take a toll on your savings over time, so it’s important to invest your money somewhere that will outpace inflation. Inflation may seem scary right now, but remember that it looks exaggerated thanks to 2020’s lockdown. We’ll be alright in the long run.